Mega888 mempunyai pelbagai lesen dari badan pengawal selia terkemuka. Ini memastikan keselamatan dan ketelusan platform mereka, menawarkan pengalaman perjudian yang menarik dan bertanggungjawab.

Memahami Platform Mega888

Mega888 adalah platform kasino dalam talian yang sangat popular di Malaysia. Ia menawarkan pengalaman berjudi yang seru dan selamat kepada pemain di seluruh negara. Mega888 menonjol dengan ciri-ciri unik dan kemudahan yang ditawarkan, menjadikannya pilihan utama bagi penggemar kasino dalam talian.

Ciri-ciri Utama Mega888

Mega888 menawarkan banyak ciri yang menjadikannya pilihan utama di Malaysia. Beberapa ciri utama termasuk:

Antara muka yang mudah digunakan dan reka bentuk yang menarik

Kemudahan muat turun aplikasi APK untuk Android, membolehkan akses mudah

Versi APK Mega888 yang asli mematuhi piawaian industri, memberikan pembayaran yang konsisten dan keselamatan maju

Kompatibiliti penuh dengan peranti iOS, memerlukan iOS 10 atau yang lebih baharu

Pelbagai jenis permainan, termasuk slot, permainan kasino tradisional, dan permainan arkad

Sistem Keselamatan dan Lesen

Keselamatan dan perlindungan pemain adalah prioriti utama Mega888. Platform ini menggunakan teknologi enkripsi canggih untuk melindungi data dan transaksi pengguna. Mega888 juga mempunyai lesen perjudian yang sah, memastikan operasinya mematuhi peraturan yang ditetapkan.

Untuk memastikan pengalaman perjudian dalam talian yang selamat dan terjamin, Mega888 menjalani audit keselamatan yang kerap. Penyokong pelanggan 24/7 juga disediakan untuk membantu pengguna dengan sebarang pertanyaan atau masalah yang mungkin timbul.

Ciri

Keterangan

Antara muka mesra pengguna

Mega888 mempunyai antara muka yang mudah digunakan dan reka bentuk yang menarik.

Kebolehcapaian iOS dan Android

Tersedia untuk kedua-dua sistem operasi, dengan versi APK untuk Android dan versi iOS yang kompatibel.

Pelbagai jenis permainan

Menawarkan pelbagai jenis permainan kasino termasuk slot, permainan tradisional dan permainan arkad.

Keselamatan terjamin

Menggunakan teknologi enkripsi canggih dan mempunyai lesen perjudian yang sah.

Kaedah Pembayaran E-wallet yang Disokong

Kasino dalam talian terkemuka di Malaysia, seperti Mega888, menawarkan pelbagai e-wallet untuk pembayaran. Ini membuat deposit dan pengeluaran lebih mudah bagi pemain. Mereka juga memastikan transaksi selamat dan perlindungan data peribadi.

Antara e-wallet yang disokong oleh Mega888 termasuk:

Touch 'n Go eWallet

Boost

GrabPay

ShopeePay

BigPay

Pengguna hanya perlu muat turun aplikasi e-wallet pilihan dan daftar akaun. Kemudian, hubungkannya dengan akaun Mega888 mereka. Kaedah pembayaran dalam talian ini memberikan kemudahan, keselamatan, dan transaksi cepat.

Dengan sokongan pelbagai e-wallet, Mega888 memastikan pengalaman bermain yang lancar dan selamat bagi pemain.

Panduan Pendaftaran Akaun Baharu

Mendaftar akaun baharu di Mega888 Malaysia sangat mudah. Anda hanya perlu mengikuti beberapa langkah sederhana. Ini membolehkan anda menikmati banyak permainan slot, kad, dan meja yang menarik.

Proses pengesahan identiti yang ketat juga memastikan keselamatan akaun anda. Ini menjadikan pengalaman bermain anda lebih selamat.

Langkah-langkah Pendaftaran

Kunjungi laman web Mega888 atau muat turun aplikasi mudah alih mereka.

Klik pada butang "Daftar" untuk memulakan proses pendaftaran akaun baharu.

Isi borang pendaftaran dengan maklumat peribadi anda dengan teliti, seperti nama, nombor telefon, dan alamat e-mel.

Cipta kata laluan yang selamat untuk memastikan keselamatan akaun anda.

Anda mungkin juga diminta untuk mengesahkan alamat e-mel atau nombor telefon anda untuk proses pengesahan.

Setelah pendaftaran selesai, anda boleh mula meneroka pelbagai permainan yang ditawarkan oleh Mega888.

Pengesahan Identiti

Untuk memastikan Mega888 memberikan pengalaman yang selamat, anda mungkin perlu mengesahkan identiti anda. Ini melibatkan mengunggah salinan dokumen pengenalan diri seperti kad pengenalan atau pasport. Tujuan utama adalah untuk memastikan anda adalah pemain yang sah dan mencegah aktiviti penipuan.

Dengan mengikuti panduan ini dan menyediakan maklumat yang tepat, anda akan dapat mendaftar akaun Mega888 dengan mudah. Anda akan menikmati permainan kasino dalam talian yang selamat.

Koleksi Permainan Slot Popular

Mega888 adalah salah satu platform perjudian dalam talian terkemuka di Malaysia. Mereka menawarkan banyak permainan slot yang menarik dan menguji. Beberapa permainan slot popular termasuk "Raja Laut," "Da Sheng Nao Hai," "Panther Moon," dan "Terumbu Dolphin."

Permainan ini menawarkan grafik menarik, tema unik, dan peluang jackpot yang menarik bagi peminat slot di Malaysia.

Mega888 juga menawarkan permainan meja dan live casino. Pemain yang mencari pengalaman perjudian dalam talian yang interaktif akan menemui kemudahan akses melalui peranti mudah alih. Aplikasi mudah dimuat turun di iOS dan Android.

Pemain baharu di Mega888 dapat menikmati banyak bonus dan promosi menarik. Ini termasuk bonus pendaftaran dan peluang untuk mendapatkan free spins. Proses pendaftaran akaun di Mega888 juga cepat dan mudah, membolehkan pemain mula bermain dengan cepat.

"Mega888 menyediakan pengalaman perjudian dalam talian yang luar biasa dengan pelbagai permainan slot yang menarik dan mengujikan."

Mega888 telah menjadi salah satu platform slot popular Malaysia yang paling diminati. Ini berkat ciri menarik dan kemudahan yang ditawarkan.

Perbandingan Platform: Joker123 vs XE88

Dua platform popular dalam perjudian dalam talian Malaysia ialah Joker123 dan XE88. Mereka menawarkan banyak permainan menarik. Namun, ada perbezaan penting antara keduanya yang perlu diketahui oleh pemain.

Kelebihan Setiap Platform

Joker123 dikenali dengan antara muka pengguna yang mudah dan banyak pilihan permainan slot. Mereka juga menawarkan permainan meja seperti blakjak dan roulette. Sementara itu, XE88 fokus pada permainan slot dengan grafik canggih dan peluang menang tinggi.

Joker123 menawarkan lebih banyak pilihan permainan meja seperti blackjak dan roulette

XE88 menawarkan permainan slot dengan grafik menarik dan peluang menang tinggi

Kedua-dua platform mempunyai sistem keselamatan yang kukuh dan penawaran bonus menarik

Pemilihan Permainan Terbaik

Memilih platform perjudian dalam talian bergantung pada jenis permainan yang disukai. Jika anda suka permainan slot, XE88 mungkin lebih sesuai. Bagi yang suka permainan meja, Joker123 mungkin lebih baik. Pilihan bergantung pada gaya permainan individu.

"Pemilihan platform perjudian dalam talian harus berdasarkan jenis permainan yang anda sukai dan gaya permainan anda."

Dengan memahami kelebihan setiap platform, pemain boleh membuat keputusan yang lebih bijak. Ini membantu memilih platform yang sesuai dengan gaya permainan mereka.

Strategi Bermain Live22

Bagi penggemar taktik Live22, menguasai strategi bermain di platform kasino langsung seperti Live22 adalah kunci untuk meningkatkan peluang kemenangan. Berikut adalah beberapa tip yang boleh digunakan untuk mempertajamkan strategi menang anda di Live22:

Kenali Permainan: Pelajari dan fahami dengan teliti setiap jenis permainan yang ditawarkan di Live22. Kuasai peraturan, strategi, dan juga peluang kemenangan untuk setiap permainan.

Urus Modal dengan Bijak: Tetapkan had perbelanjaan yang munasabah dan patuhi had tersebut. Elakkan daripada berbelanja terlalu banyak dan hilang kawalan.

Manfaatkan Bonus: Manfaatkan bonus dan promosi yang ditawarkan oleh Live22 untuk melipatgandakan modal anda. Baca syarat dan peraturan dengan teliti sebelum menggunakan bonus tersebut.

Tumpukan pada Permainan Berganda: Pilihlah permainan seperti blackjack atau baccarat yang menawarkan peluang berganda untuk memenangi lebih banyak.

Tetapkan Matlamat: Tetapkan matlamat kewangan yang realistik dan patuhi ia sepanjang permainan. Jangan sesekali terpengaruh dengan emosi semasa bermain.

Dengan mengamalkan strategi ini, pemain Live22 boleh meningkatkan peluang untuk meraih kemenangan yang konsisten dalam permainan kasino langsung. Sentiasa fokus, tenang, dan berhati-hati semasa bermain demi mencapai kejayaan yang diimpikan.

Panduan 918Kiss untuk Pemain Baharu

Permainan kasino 918Kiss semakin popular di Malaysia. Sebagai pemain baharu, penting untuk tahu cara bermain dan mengurus modal dengan bijak. Ini akan memastikan pengalaman bermain yang menyeronokkan dan berjaya.

Tips Bermain Efektif

Anda boleh bermain dengan lebih baik di 918Kiss dengan mengikuti beberapa tips berikut:

Pelajari peraturan permainan dengan teliti sebelum memulakan.

Belajar strategi asas untuk permainan pilihan anda, seperti blackjack atau poker.

Perhatikan pergerakan kad atau putaran roda untuk mengenal pola.

Tetapkan had pertaruhan dan patuhi untuk mengelakkan kehilangan wang berlebihan.

Manfaatkan bonus dan promosi untuk meningkatkan peluang menang.

Pengurusan Modal yang Bijak

Mengurus modal dengan baik sangat penting untuk pengalaman perjudian yang menyeronokkan di 918Kiss. Berikut adalah beberapa petua untuk mengurus modal anda:

Tetapkan bajet dan batasan pertaruhan yang realistik berdasarkan kemampuan kewangan anda.

Jangan bertaruh melebihi had yang ditetapkan, walaupun anda sedang menang.

Belajar untuk berhenti bermain apabila mencapai had keuntungan atau kerugian yang ditetapkan.

Elakkan daripada mengejar kerugian dengan pertaruhan yang semakin besar.

Gunakan wang tambahan, bukan wang yang diperlukan untuk keperluan harian.

Dengan mengikuti tips dan strategi ini, anda akan dapat menikmati permainan 918Kiss dengan lebih terkawal. Anda akan mendapat pengalaman yang lebih menyeronokkan sebagai pemain baharu.

Bonus dan Promosi Eksklusif

Para peminat kasino dalam talian di Malaysia suka bonus dan promosi. Platform seperti Mega888 selalu menawarkan bonus kasino dan tawaran istimewa. Ini untuk menarik pemain baru dan menjaga mereka setia.

Mega888 menawarkan promosi eksklusif seperti bonus deposit. Pemain dapat kredit tambahan apabila deposit pertama. Sebagai contoh, RM100 deposit boleh dapat RM200 kredit untuk main slot atau kasino langsung.

Mega888 sering menjalankan kempen bonus kasino seperti "Bonus Selamat Datang" untuk pemain baharu

Platform ini juga menawarkan promosi eksklusif seperti "Bonus Harian", "Bonus Putaran Percuma", dan "Jackpot Progresif"

Selain itu, Mega888 juga mempunyai program "Ahli Premium" yang memberi pelbagai tawaran istimewa kepada pemain yang aktif

Dengan banyak bonus kasino dan promosi eksklusif, Mega888 ingin memberikan pengalaman judi dalam talian yang hebat. Ini untuk pemain di Malaysia.

Sokongan Pelanggan 24/7

Di Mega888, kami tahu pentingnya sokongan pelanggan yang baik. Pasukan kami bekerja 24/7, siap membantu anda kapan saja. Anda boleh hubungi kami melalui banyak cara.

Saluran Komunikasi

Anda boleh hubungi kami lewat:

E-mel

Sembang langsung

Nombor telefon sokongan

Media sosial seperti WhatsApp, WeChat, dan Telegram

Kami cepat dan mesra dalam membantu. Kami akan segera menyelesaikan masalah anda.

Penyelesaian Masalah

Pasukan kami boleh menangani banyak isu. Anda boleh minta bantuan tentang permainan, deposit, atau masalah akaun. Kami pastikan anda puas hati.

Kami juga menerima maklum balas dari pemain. Dengan bantuan anda, kami akan terus meningkatkan perkhidmatan. Kami ingin anda menikmati bermain di Mega888.

Keselamatan dan Perlindungan Data

Di Mega888, kami tahu betapa pentingnya keselamatan kasino dalam talian dan perlindungan data peribadi pemain. Kami telah mengambil langkah-langkah keselamatan yang komprehensif. Ini untuk memastikan privasi pemain terjamin dan pengalaman bermain yang selamat.

Antara inisiatif utama kami adalah:

Penggunaan penyulitan data canggih untuk melindungi maklumat sensitif pengguna.

Infrastruktur pelayan yang selamat dan berprestasi tinggi untuk mencegah ancaman keselamatan.

Audit keselamatan dalaman dan luaran yang kerap untuk mengenal pasti dan menangani jurang keselamatan.

Kawalan akses ketat ke pangkalan data dan sistem kritikal untuk mengurangkan risiko penyalahgunaan.

Latihan komprehensif untuk kakitangan mengenai amalan terbaik perlindungan data.

Kami juga mematuhi Akta Perlindungan Data Peribadi (PDPA) Malaysia dalam pengendalian perlindungan data peribadi pengguna. Ini termasuk:

Pengumpulan dan penyimpanan data peribadi yang bertanggungjawab.

Pendedahan data hanya kepada pihak yang dibenarkan dan keperluan perniagaan.

Membenarkan pengguna mengakses, membetulkan atau meminta penghapusan data mereka.

Pematuhan kepada tempoh penyimpanan data yang ditetapkan.

Kami komited untuk terus memperkukuh keselamatan kasino dalam talian dan perlindungan data peribadi pemain Mega888. Ini adalah keutamaan kami dalam membina ekosistem perjudian digital yang selamat dan terpercaya.

Jenis Maklumat Peribadi

Penggunaan

Nama penuh, Maklumat hubungan, Tarikh lahir, Alamat kediaman

Pengesahan identiti, Pengurusan akaun

Maklumat pembayaran

Pemprosesan transaksi

Alamat IP, Maklumat peranti

Analisis dan pematuhan undang-undang

Sejarah permainan, Transaksi

Pengurusan akaun, Analisis

Panduan Menang Konsisten

Bermain di kasino dalam talian boleh sangat menyeronokkan. Namun, untuk menang secara konsisten, kita perlu strategi yang jelas. Strategi menang kasino termasuk pengurusan risiko yang baik dan mendengar tips pemain berjaya.

Pengurusan risiko sangat penting di kasino dalam talian. Tetapkan had perbelanjaan yang sesuai dan jangan lepas darinya. Jangan cuba mengejar kerugian dengan meningkatkan pertaruhan. Ini hanya meningkatkan risiko dan kurangkan peluang menang.

Kenali mekanik permainan dengan baik. Fahami cara-cara permainan dan strategi terbaik untuk setiap jenis permainan.

Manfaatkan bonus dan promosi dari platform kasino dalam talian. Bonus ini boleh meningkatkan modal anda.

Bersikap tenang dan fokus semasa bermain. Jangan terburu-buru atau membuat keputusan emosional.

Dengarkan nasihat dari tips pemain berjaya. Mereka yang sukses dalam perjudian boleh berbagi pengalaman dan strategi yang efektif. Dengan pengurusan risiko yang baik dan tips dari pemain berjaya, anda boleh meningkatkan peluang menang di kasino dalam talian.

"Strategi kemenangan yang konsisten datang dari pemahaman tentang mekanik permainan, pengurusan modal yang berhemah, dan disiplin diri yang tinggi." - Encik Azlan, Pemain Berpengalaman

Kesimpulan

Mega888 adalah pilihan terbaik bagi ramai pemain di Malaysia. Ia menawarkan ciri menarik, sistem keselamatan yang kuat, dan bonus yang menggiurkan. Ringkasan ini menunjukkan bagaimana Mega888 memberikan pengalaman bermain yang berkualiti dan selamat.

Mega888 adalah pilihan yang baik untuk pemain baharu atau berpengalaman. Ia menawarkan akses ke banyak permainan menarik, rekabentuk yang menarik, dan sistem pembayaran yang canggih. Selain itu, sokongan pelanggan 24/7 dan langkah keselamatan yang diambil memberikan jaminan keamanan.

Dengan panduan ini, pemain di Malaysia tahu lebih banyak tentang kasino dalam talian. Mega888 adalah pilihan yang berdaya saing untuk pemain yang ingin menikmati permainan kasino dan mendapatkan pulangan yang baik.

FAQ

Apakah platform kasino dalam talian popular di Malaysia?

Di Malaysia, platform kasino dalam talian yang popular termasuk Mega888 dan Joker123. XE88, Live22, dan 918Kiss juga sangat digemari. Mereka menawarkan pelbagai permainan slot dan kaedah pembayaran e-wallet.

Bagaimana perkembangan industri perjudian dalam talian di Malaysia?

Industri perjudian di Malaysia kini lebih banyak bermain dalam talian. Ini membuat permainan slot dan kasino langsung semakin popular di kalangan pemain.

Apakah ciri-ciri unik platform Mega888?

Mega888 menawarkan banyak permainan menarik dan sistem keselamatan yang ketat. Mereka juga memiliki lesen operasi yang sah. Ini menjadikan Mega888 pilihan utama bagi banyak pemain.

Apakah e-wallet yang diterima oleh platform kasino dalam talian di Malaysia?

Di Malaysia, e-wallet seperti Maybank2u, GrabPay, dan BigPay boleh digunakan di platform kasino dalam talian. Ini memudahkan pemain untuk deposit dan keluar dengan mudah.

Bagaimana proses pendaftaran akaun baharu di platform kasino dalam talian?

Untuk daftar akaun baharu, pemain perlu isi maklumat peribadi dan lulus pengesahan identiti. Ini untuk memastikan akaun mereka selamat.

Apakah permainan slot yang paling popular di Malaysia?

Di Malaysia, permainan slot yang paling dicari termasuk tema menarik dan peluang jackpot besar. Pemain dapat menikmati berbagai pilihan permainan slot di platform kasino dalam talian.

Apakah kelebihan platform Joker123 dan XE88?

Joker123 dan XE88 adalah dua platform kasino dalam talian yang sangat digemari di Malaysia. Mereka menawarkan kelebihan tersendiri, membolehkan pemain memilih platform yang terbaik untuk mereka.

Bagaimana strategi bermain yang berkesan di platform Live22?

Untuk bermain dengan baik di Live22, pemain perlu kuasai permainan kasino langsung. Mereka juga perlu mengurus modal dengan bijak dan manfaatkan peluang yang ada.

Apakah tips bermain yang efektif di 918Kiss?

Pemain baharu di 918Kiss boleh main dengan efektif dengan mengurus modal dengan bijak. Mereka juga boleh manfaatkan bonus dan promosi untuk meningkatkan peluang menang.

Apakah bonus dan promosi terkini di platform kasino dalam talian Malaysia?

Platform kasino dalam talian di Malaysia menawarkan banyak bonus dan promosi menarik. Ini termasuk bonus deposit, putaran percuma, dan promosi istimewa. Pemain boleh gunakan bonus ini untuk meningkatkan pengalaman bermain mereka.

Bagaimana sokongan pelanggan 24/7 di platform kasino dalam talian?

Platform kasino dalam talian menyediakan sokongan pelanggan 24/7. Mereka menggunakan e-mel, borang sokongan, dan media sosial untuk membantu pemain dengan cepat.

Bagaimana keselamatan dan perlindungan data di platform kasino dalam talian?

Platform kasino dalam talian mengambil langkah keselamatan yang ketat. Mereka melindungi data peribadi dan privasi pemain dengan enkripsi data dan penyimpanan maklumat selamat.

Apakah panduan untuk menang secara konsisten di kasino dalam talian?

Untuk menang secara konsisten, pemain perlu amalkan strategi pengurusan risiko yang baik. Mereka juga perlu pelajari taktik dan tips dari pemain berjaya. Pastikan disiplin dan kawalan emosi semasa bermain.

Most companies report that they would find more guidance on sustainability reporting helpful

However, the plethora of standards currently being developed can leave companies drowning in questions over which ones really matter

Stora Enso has been navigating this space for a long time and shares their experience of the process and thoughts on the current state of play

.

Играйте crash-игры Vavada. Вам предлагают выбор из множества классических азартных игр, таких как рулетка, покер, баккара, крэпс и т. д. Если вы ищете что-то уникальное, изучите варианты с инновационной механикой

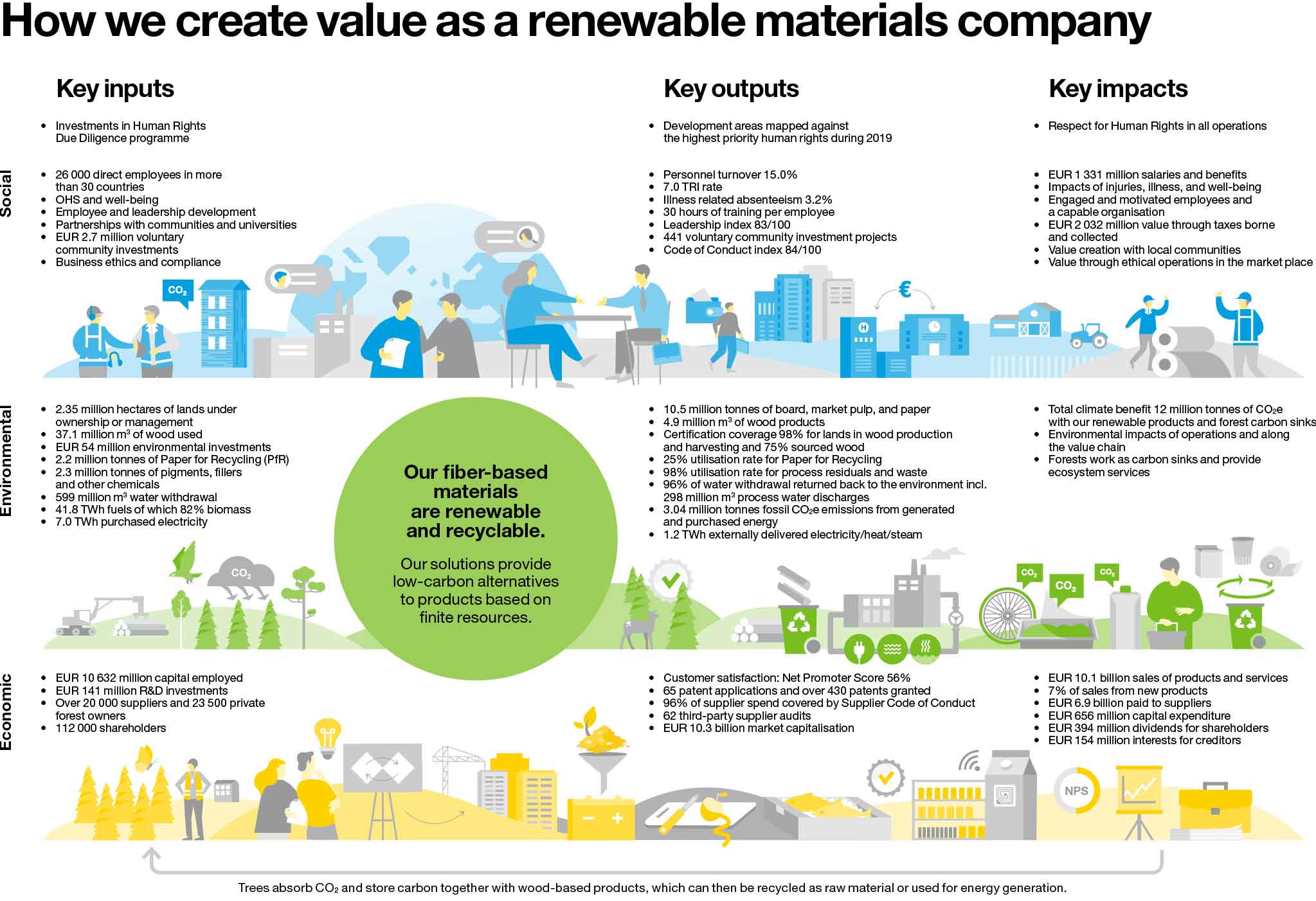

Part of the bioeconomy, Stora Enso is a leading global provider of renewable solutions in packaging, biomaterials, wooden construction and paper. The company develops and produces solutions based on wood and biomass for a range of industries and applications worldwide.

The company has a long track-record of direct communications with investors and analysts on sustainability issues comprising presentations, meetings and webinars. These are underpinned by annual reporting that aims to align with a forward view of what best practice in sustainability reporting will be.

Stora Enso's articulation of its purpose and values

Identifying that forward view, however, is not always easy. Ulla Paajanen, Stora Enso's Head of Investor Relations, shares her experience and ideas.

Q1: How does Stora Enso manage your communications on sustainability with investors?

Our most effective way of communicating with investors and wider financial markets is through personal engagements in the form of meetings and presentations virtually and physically.

Of course, with our website and annual reporting we reach wider audience, but the effectiveness is not as good as with personal dialogue.

In general, we do not find ESG ratings reports make an effective contribution to investor communications on sustainability. They tend to lack quality and comparability of the data. Also they provide little transparency on their methodology and don't make it easy for us to get feedback on the answers that we provide.

Ulla Paajanen, Stora Enso's Head of Investor Relations

Q2: Why do you engage with the development of accounting and reporting standards on sustainability? How do they help you in your communications?

To some degree standards are inevitable. The growth of passive investment and quants-based investment strategies, (involving new technologies) , means that there have to be standards if we are to maximize the benefits and avoid unintended consequences.

Companies also need to be involved in the standards development process to ensure that that the standards that are developed align with industries, markets and best sustainability practice.

At Stora Enso, we have a particular interest in being involved in the process as interest in our sustainability performance is growing strongly amongst mainstream investors and we have a positive story to tell as we are one of the few companies in the market with a positive carbon footprint.

Q3: What problems remain with the standards?

The problems at the moment are that they are still under development and will be still for some period of time. Financial accounting standards have been under development since middle ages and are still evolving with time and as the world around us changes.

So, I predict that we see the same development with sustainability standards. However, it should not take 500 years to have them ready thanks to the modern-day technology and science.

That said, even when global sustainability or ESG standards frameworks are ready, it is only reasonable to expect that they will continue to evolve with time as our understanding of ESG factors and how to measure them improves.

Q4: Which standards are highest priority for you and why?

SASB

We see SASB as important for a number of reasons:

First, because some of our largest institutional investors are strong supporters of it

Secondly, because we receive a plethora of requests from investors and from ESG ratings agencies and we think that SASB represents the best opportunity to align these into one coherent framework.

TCFD (Task Force on Climate Related Financial Disclosures)

Again, some of our largest investors are active supporters of the TCFD - so we prioritise this.

Of course, climate-related disclosure is important for Stora Enso since our activities mitigate climate change. We are one of the largest private forest owners in the world. So, we manage the carbon sinks that these forests offer and the carbon remainsstored in the products that we produce through their lifecycle.

Therefore, it is important that we measure this impact in correct manner. Poor measurement and poor reporting in this regard will lead to a distortion in the world's climate management efforts.

EU Taxonomy (for sustainable activities)

The EU Taxonomy is clearly a massive classification system including environmentally sustainable economic activities, which is in the development phase especially in our industry sector.

However, Rome wasn't built in a day and the delegated act with taxonomy criteria for forestry has been delayed until April.

Stora Enso continues to make representations to explain and inform member states and the EU Commission on the Forestry sector's contribution to tackling climate change. Over 46, 000 responses from a wide variety of stakeholders have been sent to the EU Commission which is now finalising the review and analysis of this feedback, including with regard to the comments received by Member States.

IFRS

We have participated in the consultation from IFRS on accounting standards for sustainability. While these initially focused on carbon, we are encouraging IFRS to broaden their scope to include wider relevant ESG parameters. We are also encouraging them to build on existing standards rather than to reinvent the wheel.

Q5: Practically, how do you keep up to date and engage with standards development?

There are a variety of different ways of staying engaged - depending on the standard.

We participate in consultations and working groups. We also undertake our own analysis on how the standards being developed will affect the way that we report on our own business activities.

For example, the latest participation was to give feedback to SASB’s Human Capital standard development.

This helps us to comment on standards as they are being developed and then implement them promptly if / when they are agreed.

For SASB, in particular, I have been a member of SASB’s Standards Advisory Group (SAG) since 2019.

Q6: How do you think the emergence of global frameworks will affect the sustainable investment research process?

I sincerely hope that unified standards around sustainability data will enable the ESG ratings agencies to become more like 'sell-side' sustainability analysts whereby they:

Do not require us to complete questionnaires or correct their own data-gathering - can you imagine Morgan Stanley allowing us to fill in the reports that they write on us?

Take full responsibility for the data within reports and the analysis conducted around it

Ultimately, I hope that this will enable ESG ratings firms to add value through their analysis of data rather than simply from the collection of data.

Support

Sustainable-IR thanks Ulla Paajanen of Stora Enso for her support in writing this case study.